1. Executive Summary

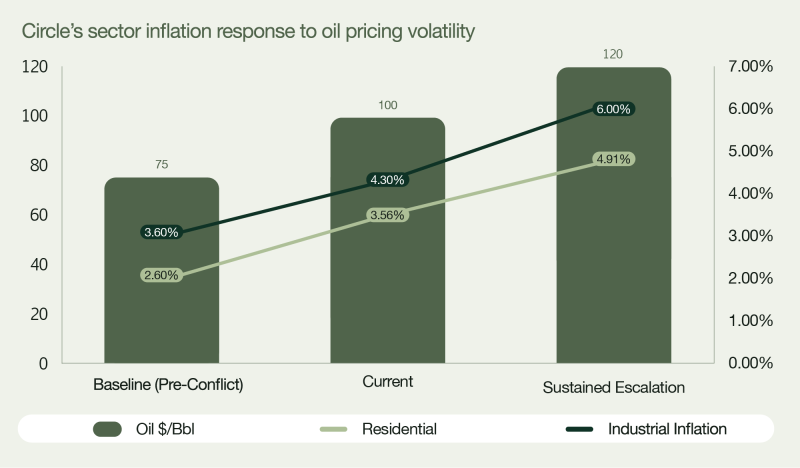

The UK construction market has entered a period of relative stability following the extreme volatility experienced between 2021 and 2023. Material price inflation has increased to approximately 3.6% year-on-year; however, this stability remains fragile, with a risk that prolonged conflict will push blended construction inflation to 5%, with overall cost levels still more than 40% above pre-pandemic benchmarks.

Recent geopolitical tensions involving Iran have reintroduced uncertainty into global energy markets. Brent crude increased from approximately $82/bbl in January 2026 to peaks above $110/bbl in Q1, while UK gas prices have risen from around £0.75/therm to circa £1.10+/therm.

This shift is significant. The market is no longer primarily demand-led; instead, energy is re-emerging as the key driver of cost risk. While a return to extreme inflation is not anticipated, volatility is likely to increase, particularly across energy-intensive materials and MEP packages.

Early supplier responses suggest this pressure is already feeding into the market, with increases typically ranging from 5% to 20% across key material groups in recent weeks.

2. Scenario Analysis: Energy Market Impact

Note: These scenarios assume no major supply chain collapse or manufacturing shutdowns. A severe disruption (e.g., prolonged Strait of Hormuz closure) could produce double-digit inflation in energy-intensive trades.

While the scenarios above reflect current macro energy pricing assumptions, emerging supply chain behaviour suggests that the scenarios above are already under upward pressure. Recent supplier announcements across concrete (5–9%), steel reinforcement (up 15–25% since early March), insulation (5–20%), and polymers (6–20%) indicate that cost increases are being implemented ahead of full energy market stabilisation.

This early response is consistent with previous inflation cycles, where manufacturers and suppliers price in anticipated energy cost increases rather than reacting purely to spot rates. As a result, there is a heightened risk that inflation outcomes track toward the upper end of the ranges set out above.

3. Energy Cost Transmission into Construction

Energy price movements feed into construction costs through several key mechanisms:

- Diesel & logistics: A $10/bbl increase in oil typically results in a 3–5% increase in diesel costs

- Manufacturing inputs: Steel, cement, bricks, and glass production remain highly dependent on gas and electricity pricing

- Petrochemical products: Insulation (PIR, EPS), plastics, and bitumen are directly linked to crude oil movements

- Imports & freight: Higher fuel costs increase shipping rates

These effects typically feed through into construction pricing within 2–4 months.

This is now being evidenced in the market. Major suppliers have implemented increases across plasterboard (4–8%, effective May–June 2026), mineral wool insulation (3–6%, effective July 2026), and chemical products (+3.5% from May), reflecting rising input costs across energy and petrochemical supply chains.

4. Sector Impact

4.1 Residential Construction (BTR, PBSA, Co-living)

Residential construction continues to face a combination of subdued demand and persistent cost pressure. While inflation has moderated, cost levels remain structurally elevated.

Labour shortages across key trades continue to underpin inflation, particularly in bricklaying, carpentry, and MEP installations. Building services packages remain the most significant source of cost pressure, with copper prices still over 35% above April 2025 levels, maintaining upward pressure on electrical and mechanical systems.

In addition, regulatory and compliance requirements, particularly around fire safety and building performance, are continuing to add cost to schemes.

Energy volatility introduces further upside risk. Residential schemes are particularly exposed through insulation and internal material packages, with recent increases ranging from 5% to 20% depending on product type.

Outlook: Residential inflation is expected to remain in the 3.5–4% range in the near term, with potential to increase toward 4–5% should energy prices remain elevated.

4.2 Industrial & Advanced Manufacturing

Industrial and logistics development continues to benefit from strong structural demand. However, this sector carries a higher exposure to cost volatility due to its reliance on energy-intensive materials and complex MEP systems.

Recent increases in key metals have materially impacted project costs. Aluminium remains approximately 13% above February levels, while copper continues to sit at historically elevated levels. Steel markets have also shown renewed volatility, with reinforcement rates increasing by approximately 15–25% since early March.

Contractor capacity, particularly within specialist MEP trades, remains constrained, further amplifying pricing pressure.

Energy costs remain a critical variable, with steel fabrication, precast concrete production, and mechanical equipment manufacturing all highly sensitive to gas and electricity pricing.

Outlook: Industrial construction is expected to experience inflation at the upper end of the 4.0–5.0% range, with higher risk for complex, large-scale, or MEP-intensive schemes.

4.3 Single-Family Housing

Single-family housing remains the most cost-sensitive segment of the market, with tighter margins and greater exposure to subcontractor pricing and availability.

Although overall material inflation has stabilised, key inputs are seeing renewed upward pressure. Concrete and aggregate suppliers have recently issued increases ranging from 5% to 9%, which is particularly impactful given the volume usage within housing.

At the same time, supply chain fragility continues to present a challenge. Approximately 3,900 construction firms became insolvent in the year to December 2025, with over half within specialist trades critical to housing delivery.

This reduction in capacity is contributing to increased pricing pressure and delivery risk.

Suppliers of plastic pipework and drainage systems have also announced increases of 6–20%, reflecting exposure to petrochemical inputs and reinforcing the sector’s sensitivity to energy movements.

Outlook: Inflation is expected to align broadly with residential averages, but with greater volatility and heightened viability risk, particularly for smaller developers.

5. Material Cost Pressures: Key Watchpoints

While overall material price inflation has moderated, several categories are now showing renewed upward movement.

Energy-intensive materials remain highly sensitive to pricing shifts. Recent increases include aggregates and concrete (5–9%) and continued upward movement in steel reinforcement (15–25% since early March).

Metals continue to represent a key risk area. Copper remains over 35% above 2025 levels, driving MEP cost pressure, while aluminium pricing remains elevated and continues to impact façade systems.

Petrochemical-derived products are seeing some of the most pronounced increases, with insulation (5–20%), polymers (6–20%), and chemical products (+3.5%) all reflecting rising oil-linked input costs.

Finishes and drylining materials are also seeing upward pressure, with major manufacturers including Knauf, Etex (Siniat), and British Gypsum announcing increases of 4–8% effective May–June 2026.

The Mineral Products Association has also flagged broader concerns around price escalation and availability.

Across all sectors, MEP packages and energy-linked materials now represent the primary source of construction cost risk.

6. Conclusion

The UK construction market has achieved a degree of stabilisation, but this remains fragile and highly sensitive to external shocks. Energy volatility is now the principal driver of inflation risk.

Recent supplier increases, typically in the range of 5% to 20% depending on material, indicate that cost pressures are already feeding back into the supply chain.

If sustained, elevated oil and gas prices could push construction inflation back toward 4–5% for residential and 5–6%+ for industrial sectors.

In this environment, proactive procurement strategies, early contractor engagement, and robust cost planning will be critical.